-

-

Please adjust the volume.

2025 Business Results

Greetings everyone.

I am Jerry Kang, head of KBFG IR team.

We will now begin the 2025 business results presentation.

Thank you very much for participating in today's earnings release. We have here with us executives from the group, including CFO, Sang Rok Na.

And first, our group CFO will cover 2025 business results. After that, we will have a Q&A session I will now invite our group CFO to walk us through 2025 business results.

Greetings everyone. I am KBFG CFO, Sang Rok Na.

Thank you very much for joining our 2025 business results presentation.

Before proceeding with the business results, I'll briefly share some of our key performance highlights.

2025 was a year of unprecedented volatility in the financial market. As volatility in the exchange rate and market interest rates widened, the influence of external factors intensified. Economic recovery was somewhat delayed, and a challenging operating environment continued with asset quality pressures.

On the other hand, as government policies materialize and discount factors for the domestic market became resolved partially. The capital market is gaining unprecedented momentum toward the 5,000 era in a situation where diverse variables and new trends are intertwined.

With our stable portfolio and consistent risk management policies, is absorbing external uncertainties. And we are working hard to expand non-banking earnings contribution and to shift to a business structure focused on the capital market.

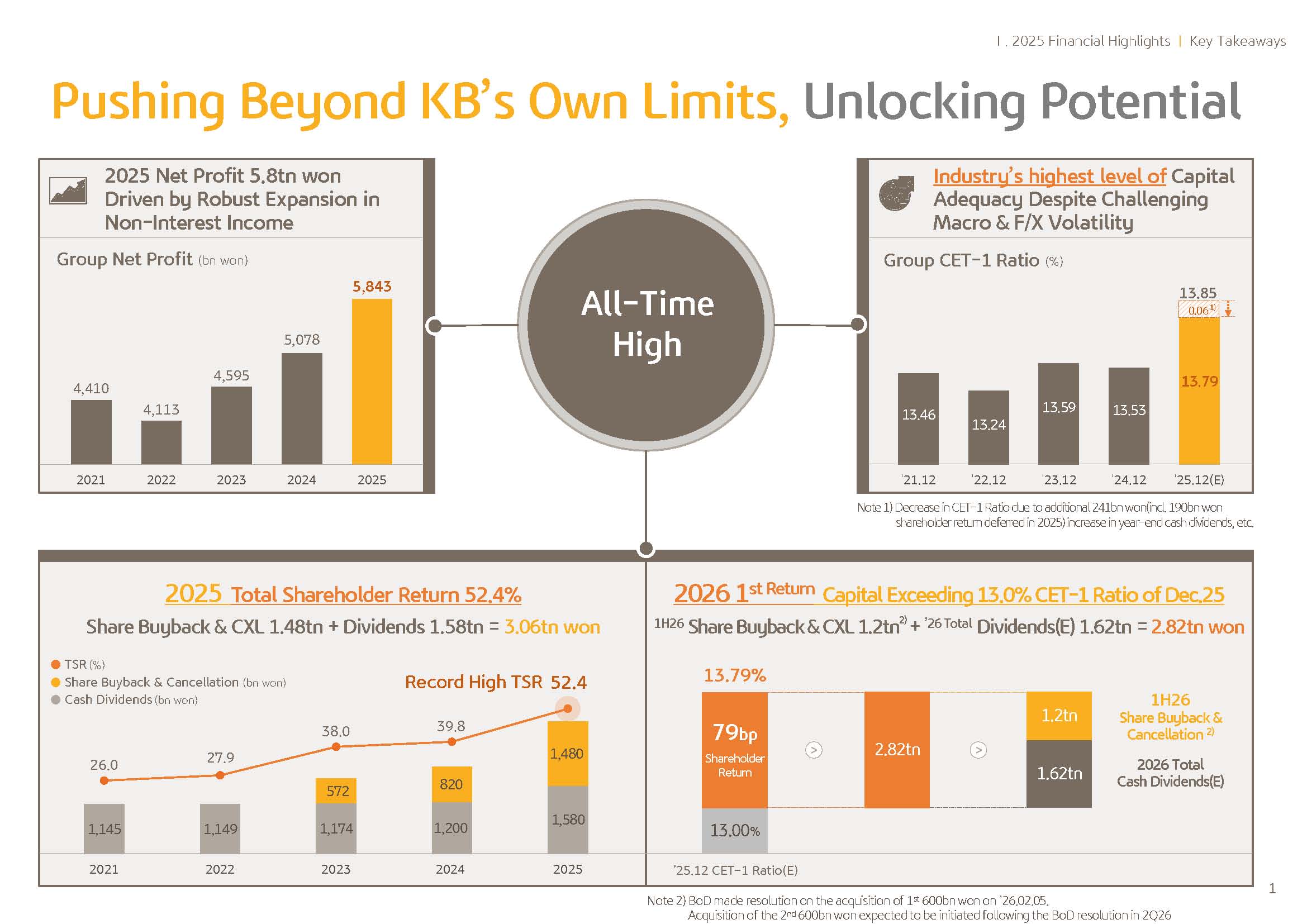

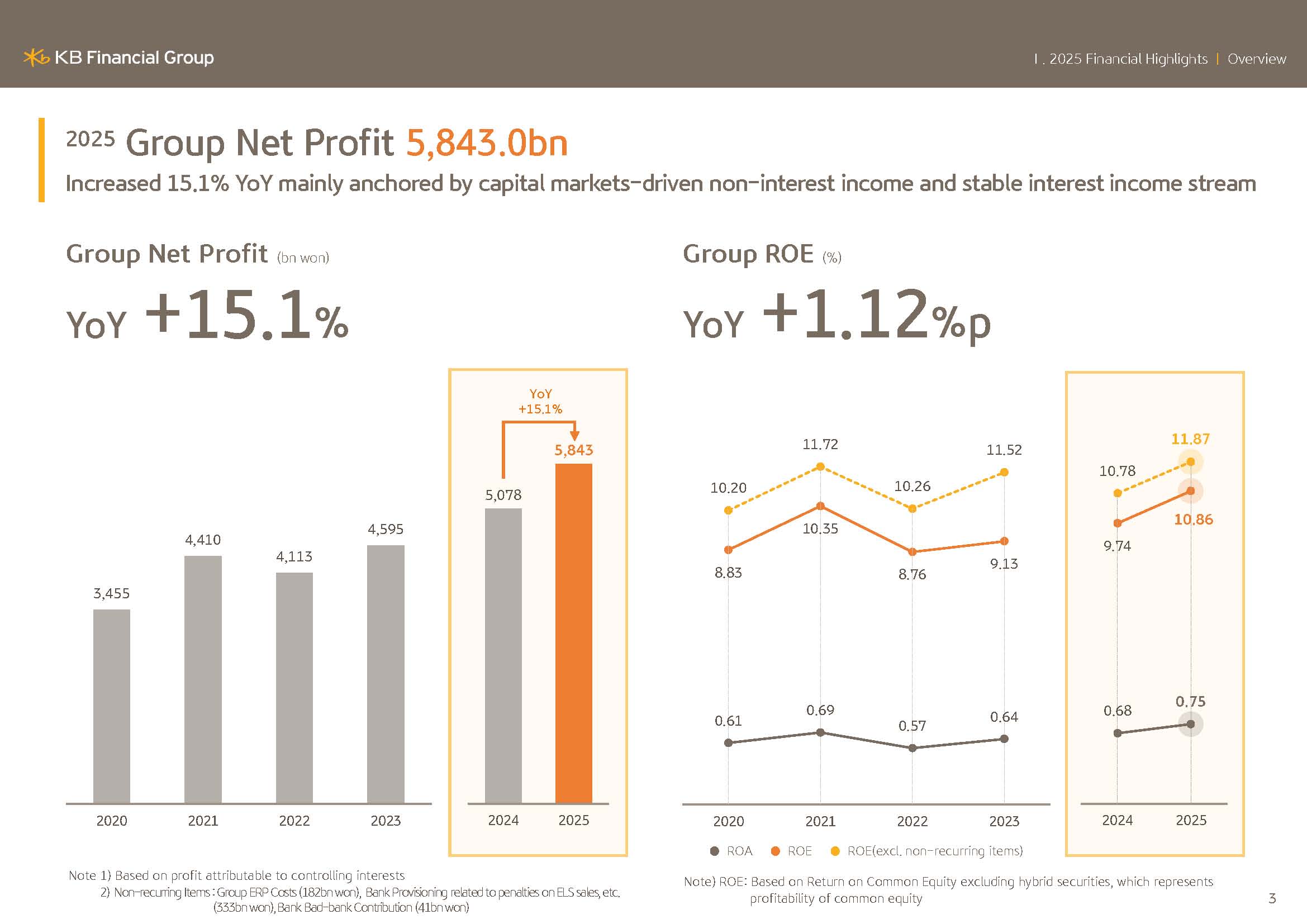

Added to these strategic efforts as a result of the fading away of sizable one-off effects, including 2024 ELS customer compensation costs, 2025 net profit posted KRW5.8 trillion, a 15.1% increase and improved our robust profit generating capacity.

On the other hand, the resolved to approve a year-end cash dividend of KRW1,605 per share, amounting to a total of KRW575.5 billion. Accordingly, the 2025 total cash dividend amount stands at KRW1,580 trillion, an increase of approximately 32% compared to the previous year.

The 2025 dividend per year, including previously paid quarterly dividends, recorded a total of KRW4,367, marking a significant increase of approximately 37.6% YoY.

The total year-end cash dividend amount includes an additional KRW240.5 billion on top of the existing 2025 quarterly uniform dividend amount.

This reflects our efforts not only to meet the corporate eligibility criteria for separate taxation on dividend income, but also our efforts to reevaluate our shareholder return mixed in line with the normalization of our PBR, which has recently surpassed 0.8 multiple while striving to achieve an industry-leading dividend payout ratio.

According to our shareholder return framework linked to our CET1 ratio, 2025 total shareholder return ratio booed 52.4%, a 12.6%p increase YoY, and also achieved an industry-leading level in both shareholder return ratio and scale.

In addition, we efficiently managed to accumulated capital and maintained industry's highest level capital adequacy level, and 2025, an anticipated CET1 ratio is.

Expected to be 13.79% and demonstrated significantly enhanced capital management capabilities, taking into account the downward impact of approximately 6 bp rising from the KRW240.5 billion of additional cash dividend amount, the effective 2025 and CET1 ratio can be considered to have remained at a high level of approximately 13.85%.

A portion of this additional cash. Dividend amount utilize KRW190 billion of deferred shareholder return for 2025. Next, I will cover details of our 2026 first phase of shareholder returns.

The funding for total shareholder returns in the first half of the year amounts to a total of KRW2.82 trillion in capital, corresponding to 79 bp above last year's ratio of 13%. It has already reached more than 92% of the total annual shareholder return of the previous year and has been expanded on a proactive basis.

Of this amount, KRW1.62 billion will be returned as total cash dividends for 2026, while the remaining KRW1.2 trillion will be returned through first-half share buyback and cancellations.

Accordingly, the resolved to conduct KRW600 billion of share buyback and cancellation, which is the first round of share buyback and will commence immediately after this earnings release. The remaining KRW600 billion is scheduled to be repurchased during the second quarter following an additional resolution upon the completion of the first round.

Also separate from this regarding the tax exempt dividends that have garnered significant market interest, we are actively reviewing the procedures for implementation, including the submission of agenda items to the GSM and plan to proceed accordingly.

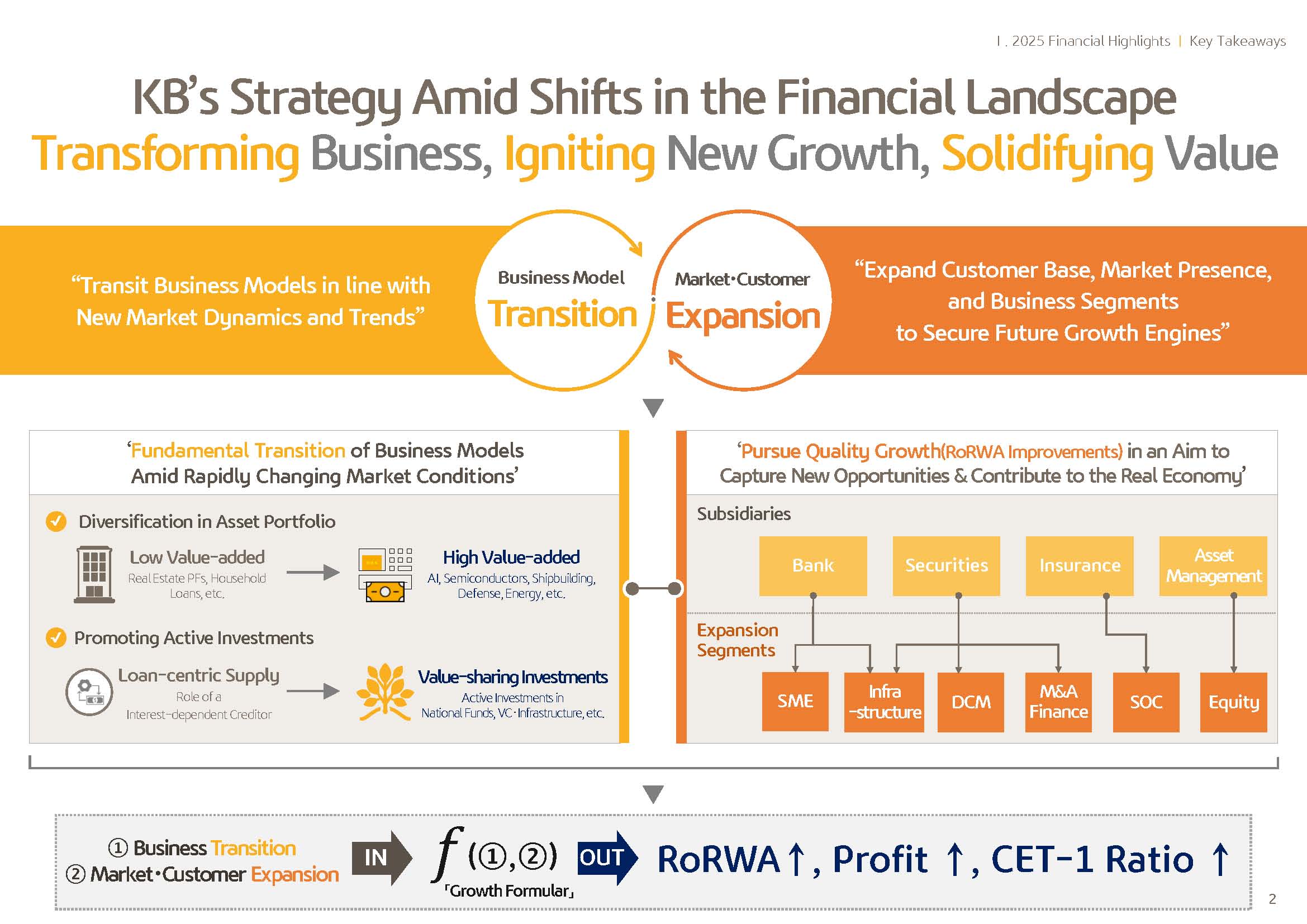

This year, under the government's economic stimulus policy stance, including productive finance, the role of financial institutions in enhancing the dynamism of the real economy is expected to expand based on our group's diversified portfolio by proactively allocating resources to high value-added areas such as AI semiconductors and innovative SMEs, fundamentally transforming the group's business model and to secure future growth engines we will continue to expand our customer base and business scope and seek to preemptively seize new opportunities amid a rapidly changing financial environment.

Centering on subsidiaries with competitiveness in corporate banking and capital market business, we will identify and preempt additional growth areas and thereby fill the foundation for future growth engines and at the same time evolve into a reliable partner that directly contributes to the real economy of the nation.

Through these management strategies of transformation and expansion, we plan to further enhance shareholder and corporate value by solidifying our profitability and earnings base while improving capital efficiency.

Next, I will cover KBFG business results.

First, our key words of 2025 group business results are as follows.

First, the full normalization of bank earnings, which has been somewhat subdued due to 2024 one-off factors.

Second, a business portfolio well prepared for the money move trend toward capital markets, as demonstrated by a significant improvement in non-interest income.

Third, enhancing cost efficiency through group-wide cost management efforts and optimal resource allocation.

Fourth, while maintaining the broad framework of KB's proprietary shareholder return formula, this can be summarized as a flexible response aimed at maximizing shareholder and investor value, including a proactive expansion of the scale of shareholder returns and the achievement of a total shareholder return ratio at the highest level in the industry.

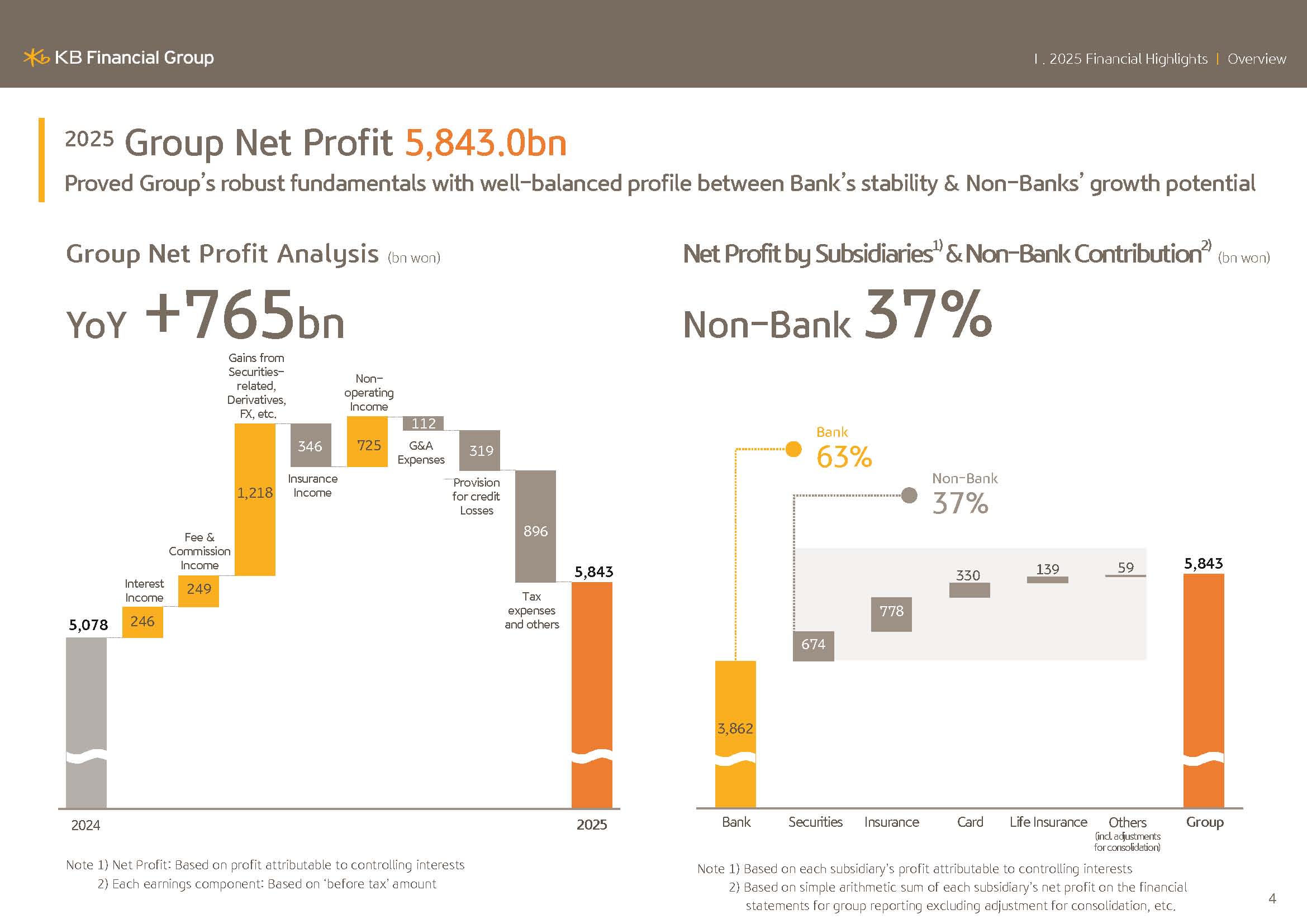

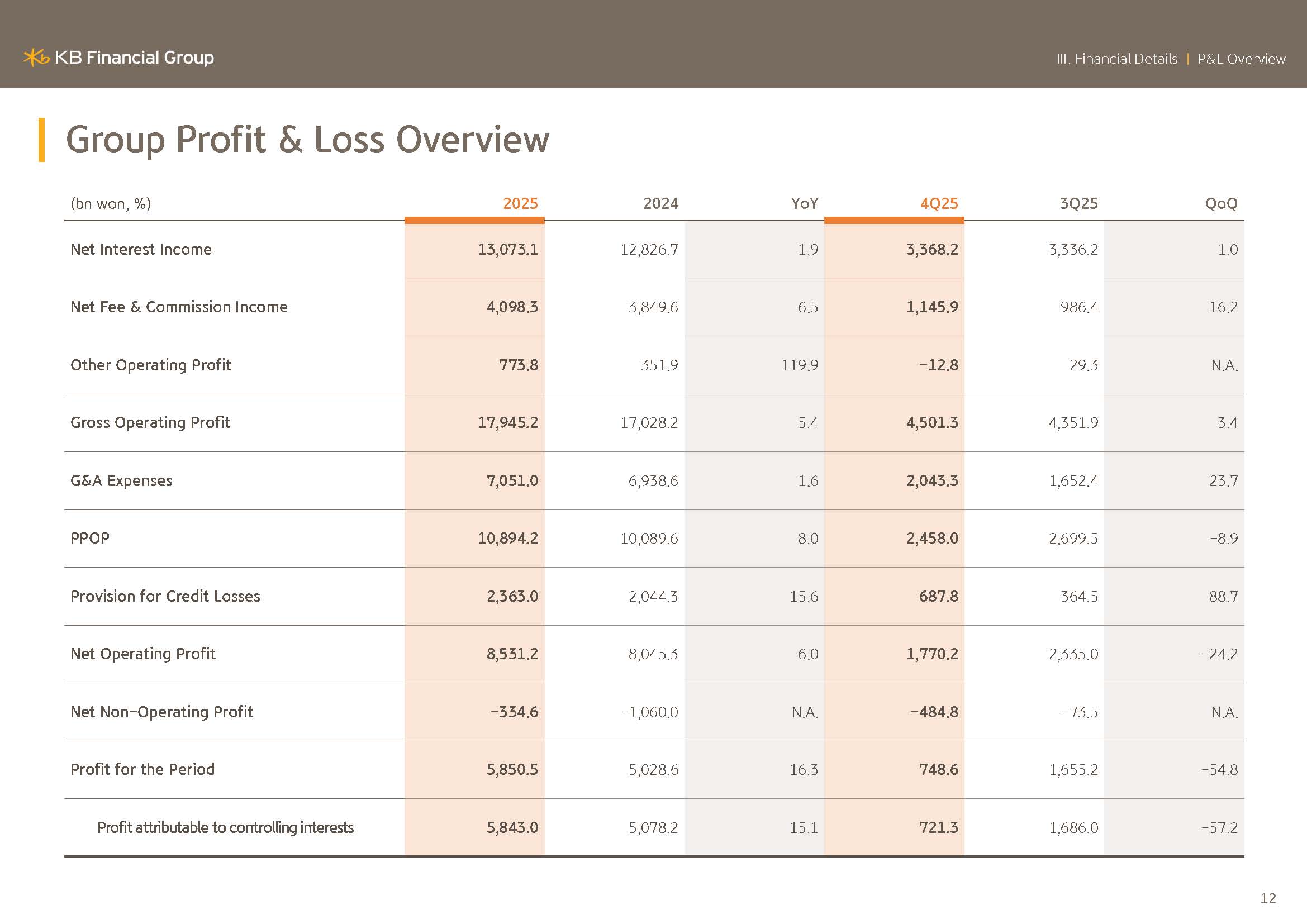

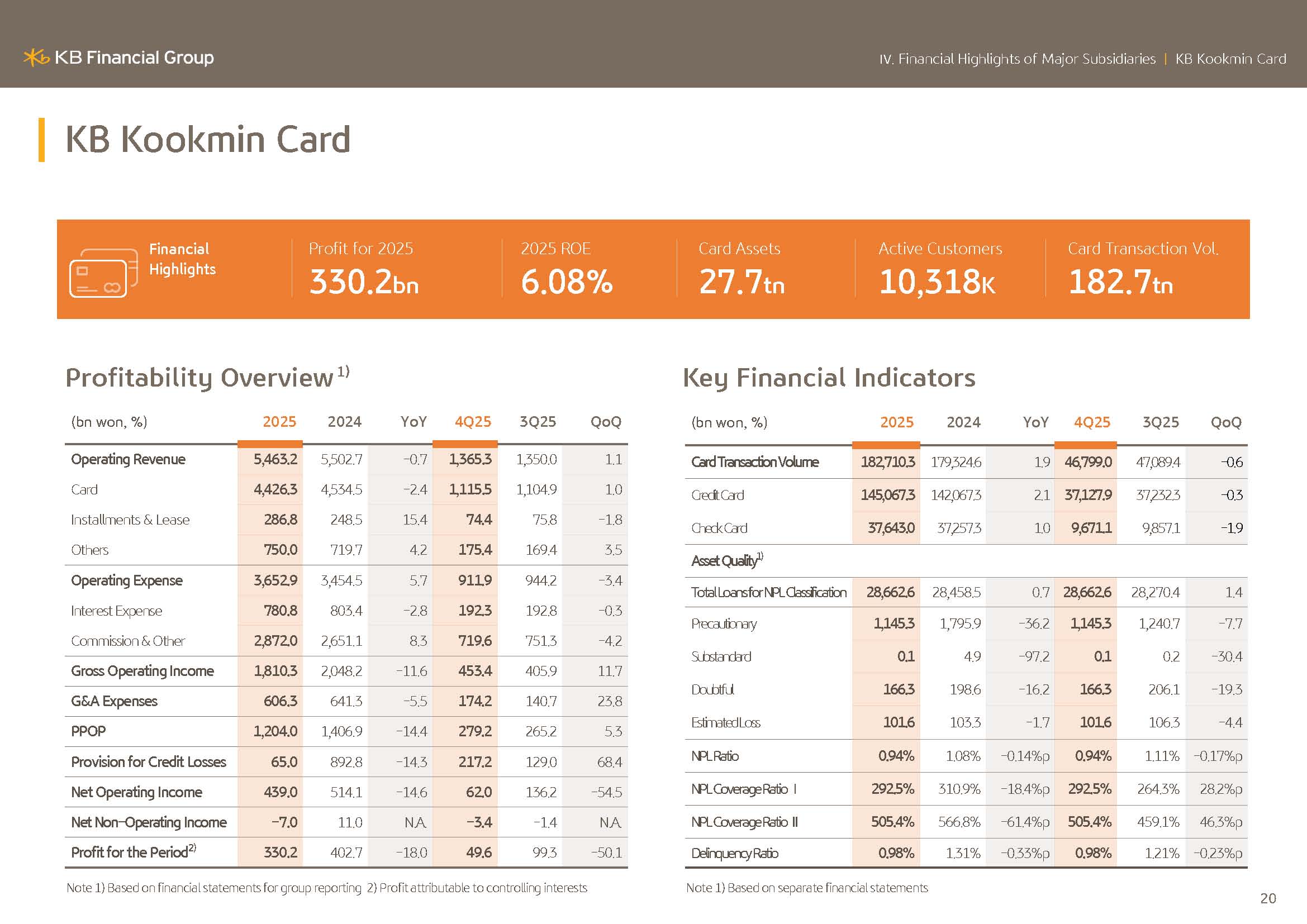

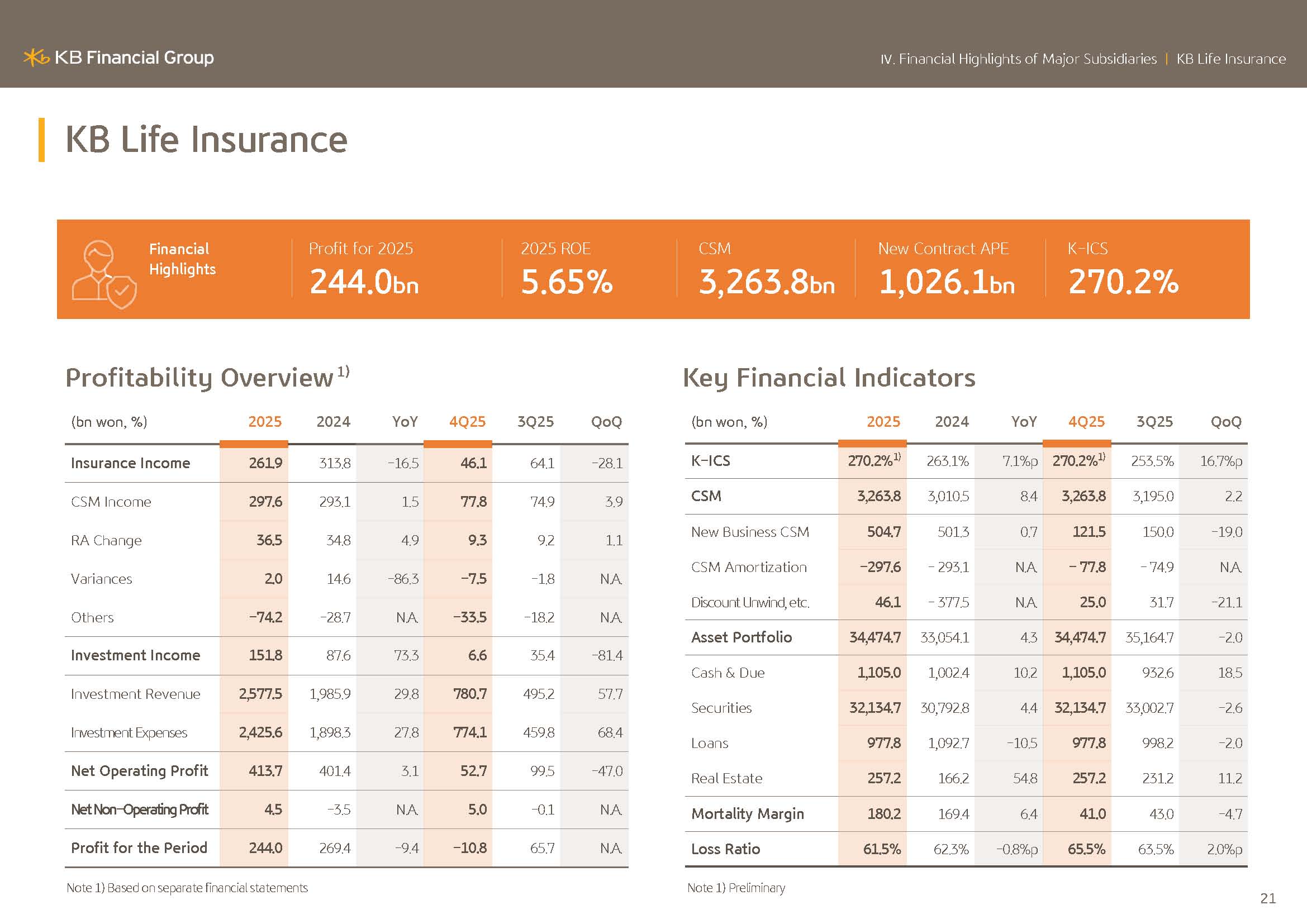

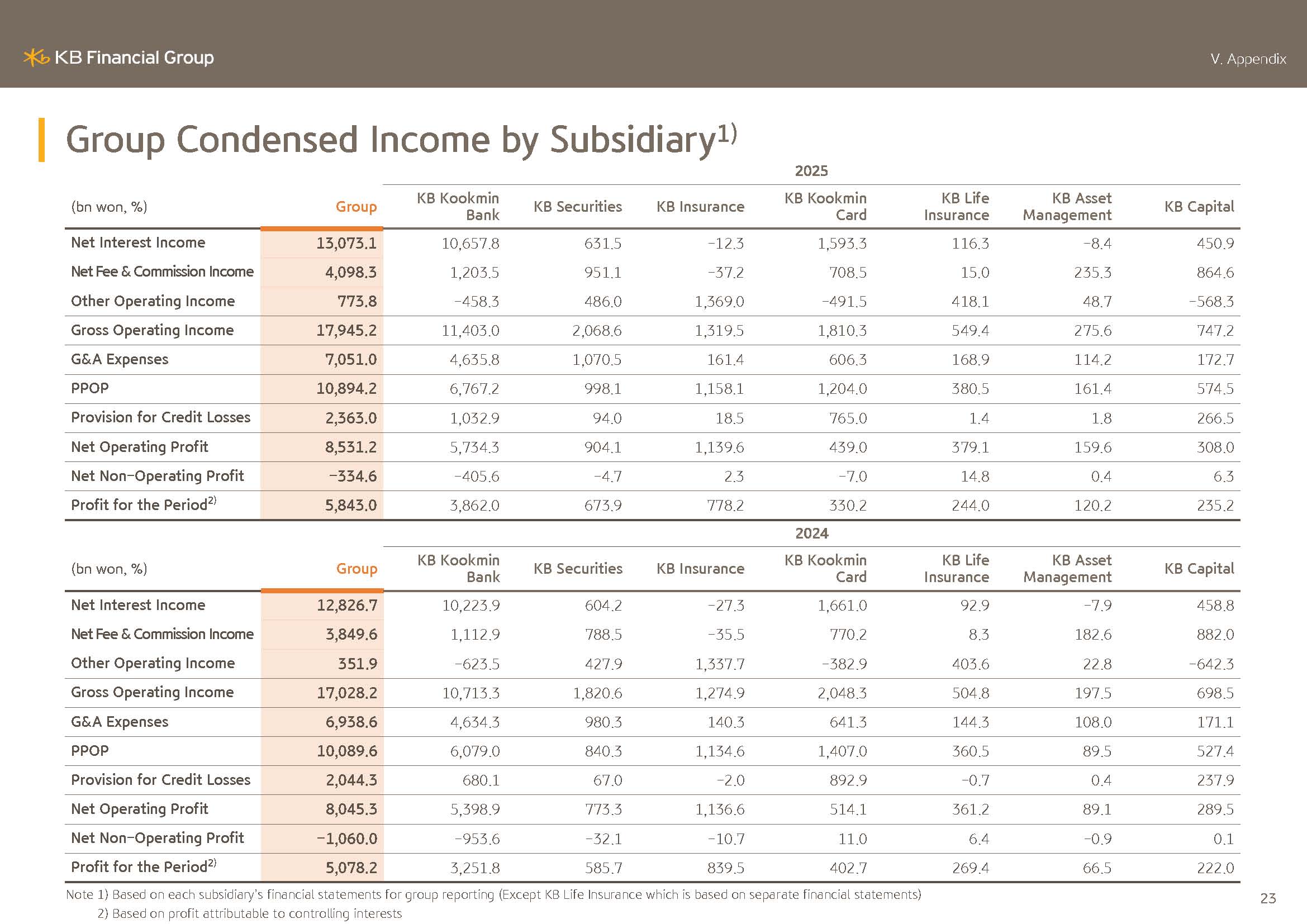

As aforementioned, our group's 2025 annual net profit posted KRW5.843 trillion, and despite unfavorable conditions such as increased volatility in exchange rates and interest rates, earnings of core subsidiaries, including banks and securities expanded.

In particular, the group's earnings power expanded as non-interest income grew significantly driven by capital market-related gains.

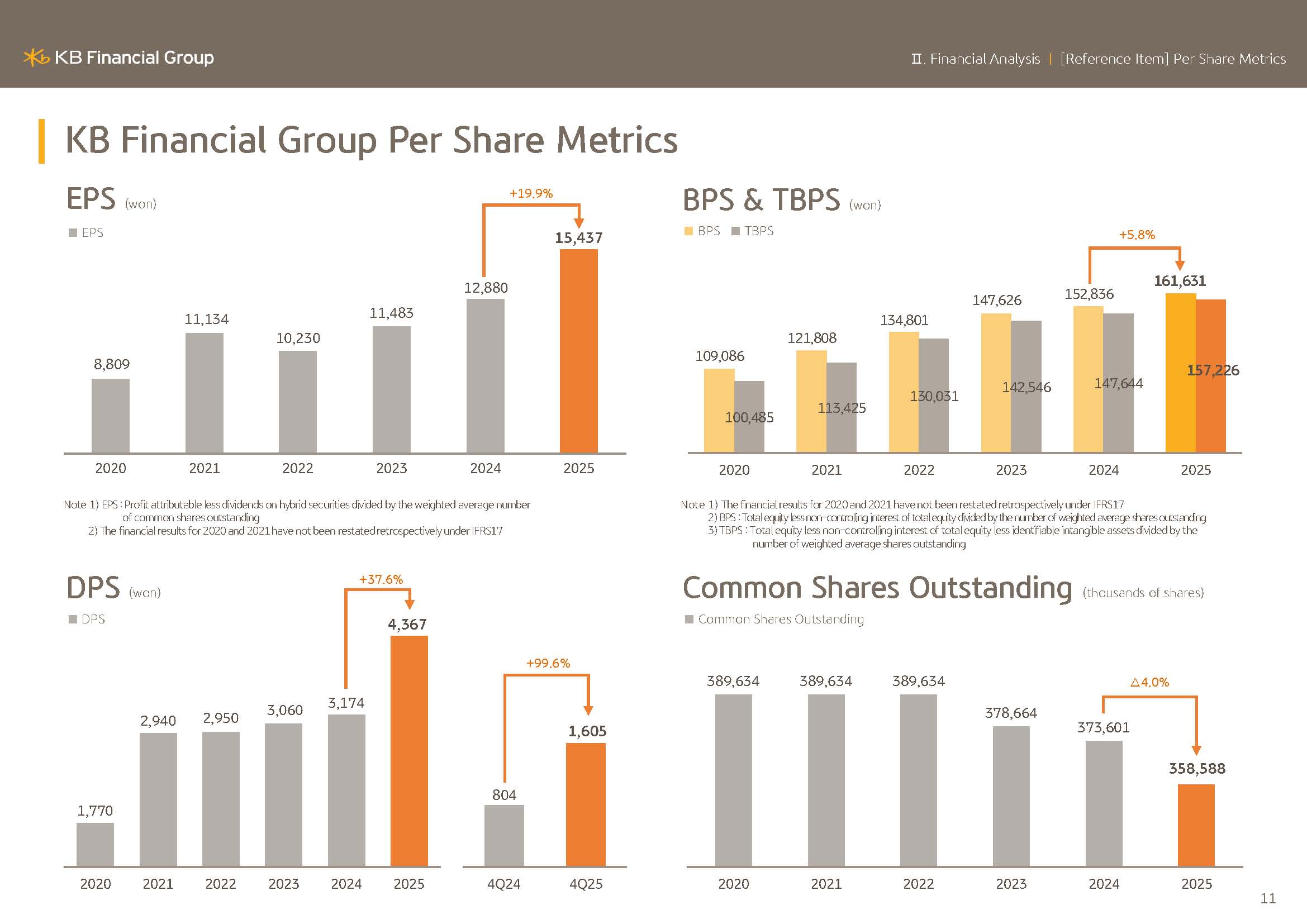

In addition, 2025 ROE posted 10.86%, a 1.1%p increase YoY, and the basic EPS earnings per share was KRW15,437, representing an approximate 20% increase YoY.

On the other hand, for Q4 net profit with a reflection of sizable one-off items including group ERP costs and provisioning for penalties including ELS as well as seasonal contraction in insurance performance, it declined significantly QoQ.

Now, I will cover business results in more detail.

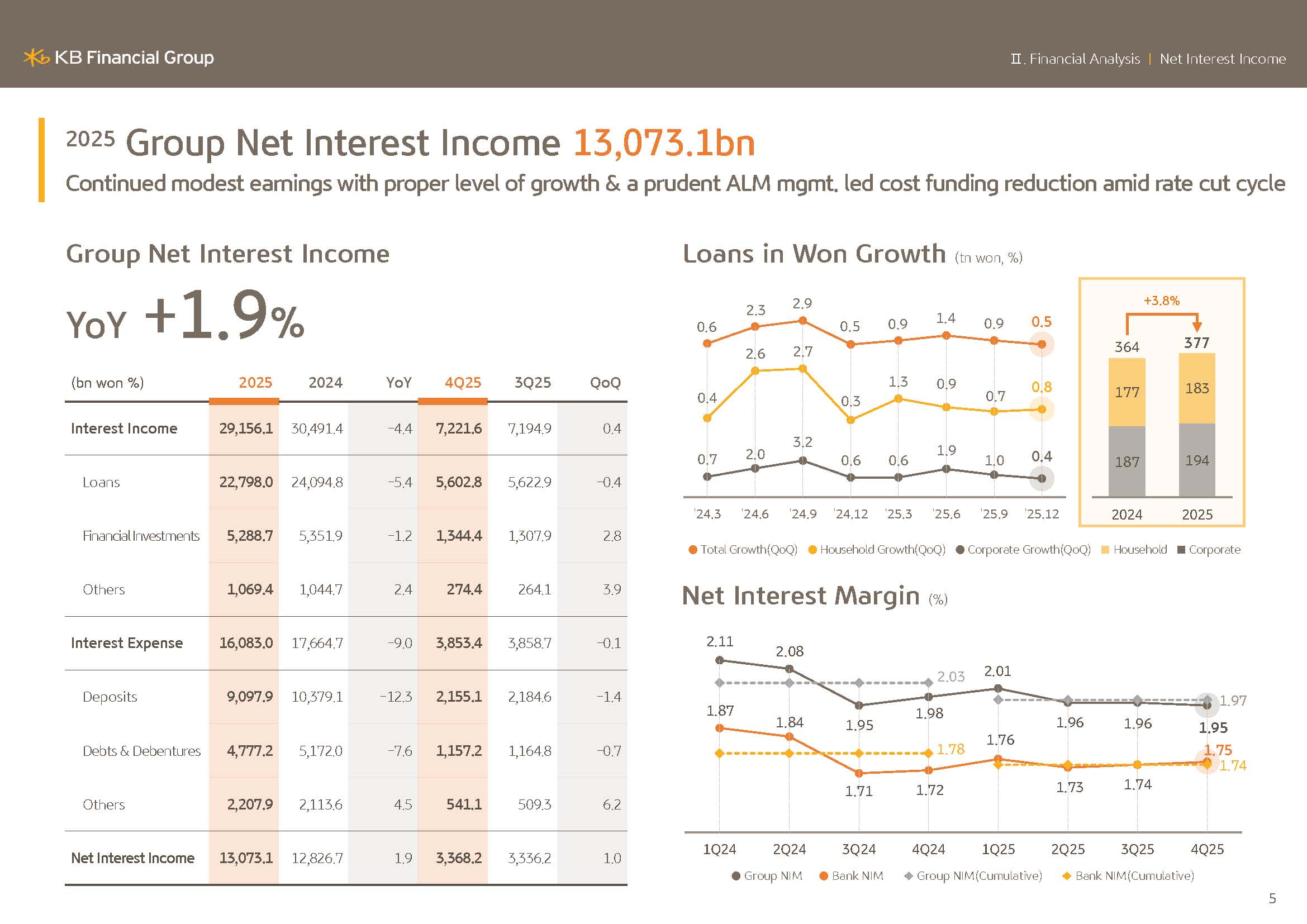

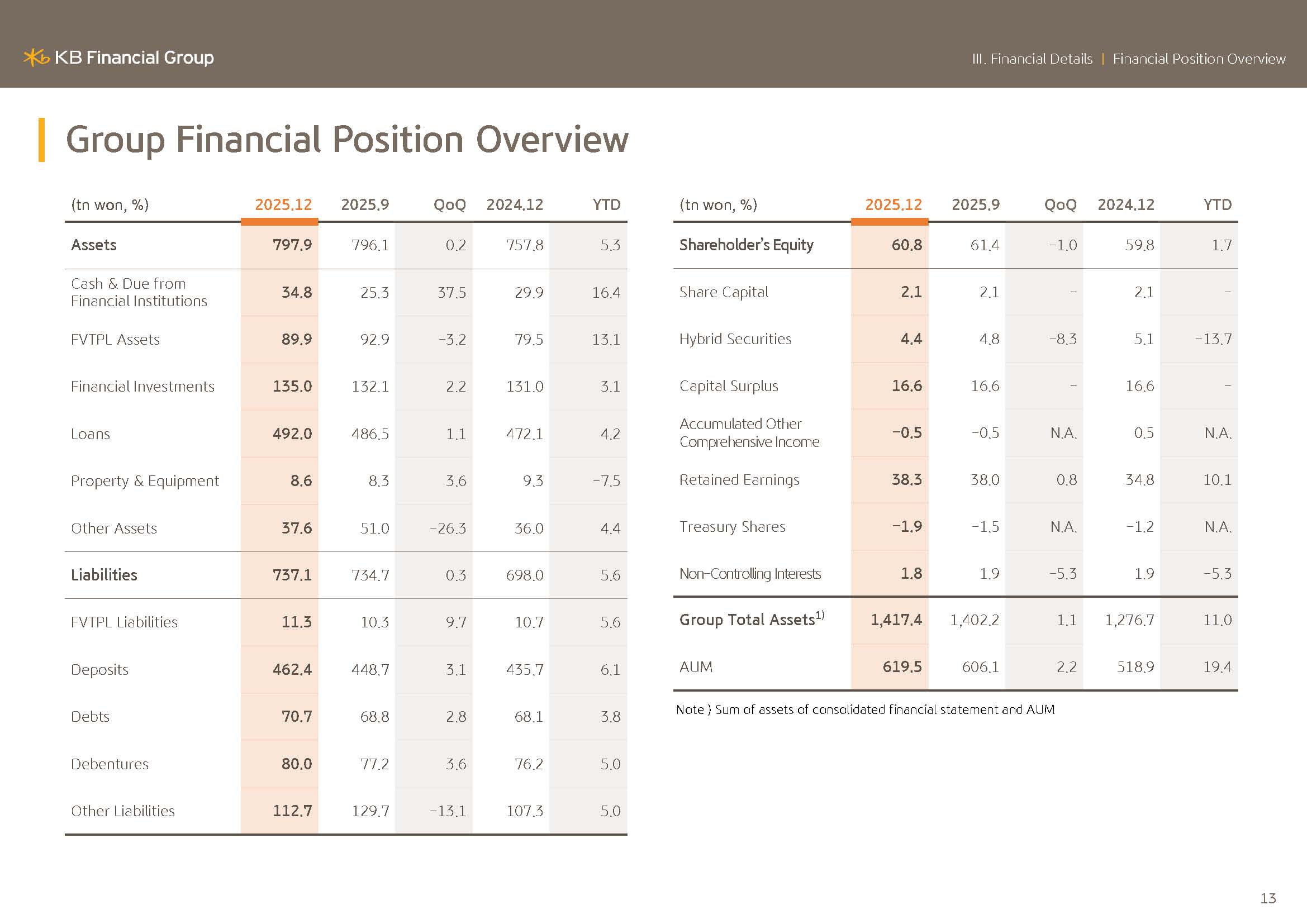

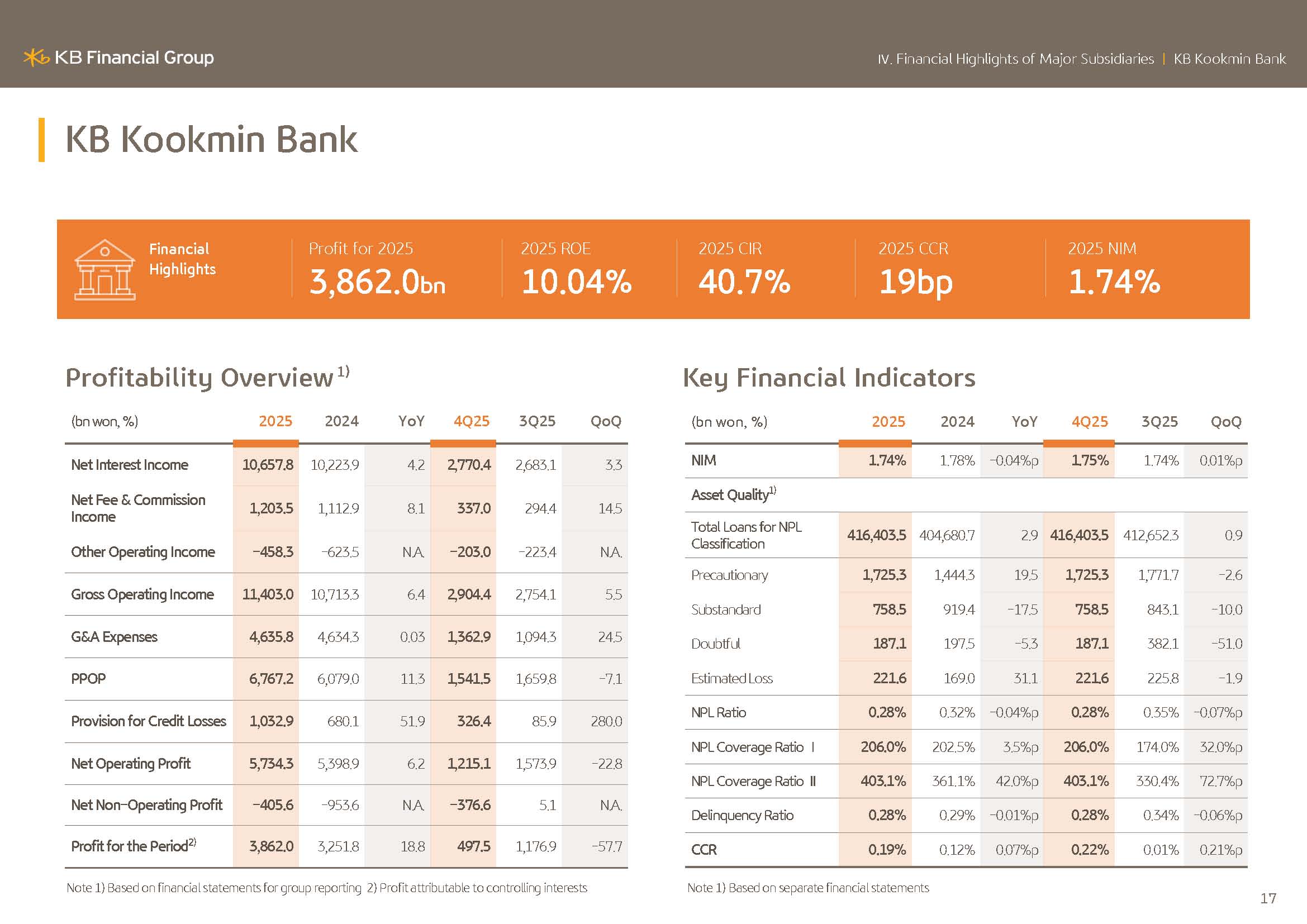

In 2025, the group's net interest income amounted to KRW13.731 trillion, increasing slightly by 1.9% YoY.

This is attributed to improved profitability despite concerns over margin pressure from the base rate cut cycle that continues through the first half, driven by growth in the average balance of the bank's loan assets and reduced funding costs through the policy to expand our core deposits.

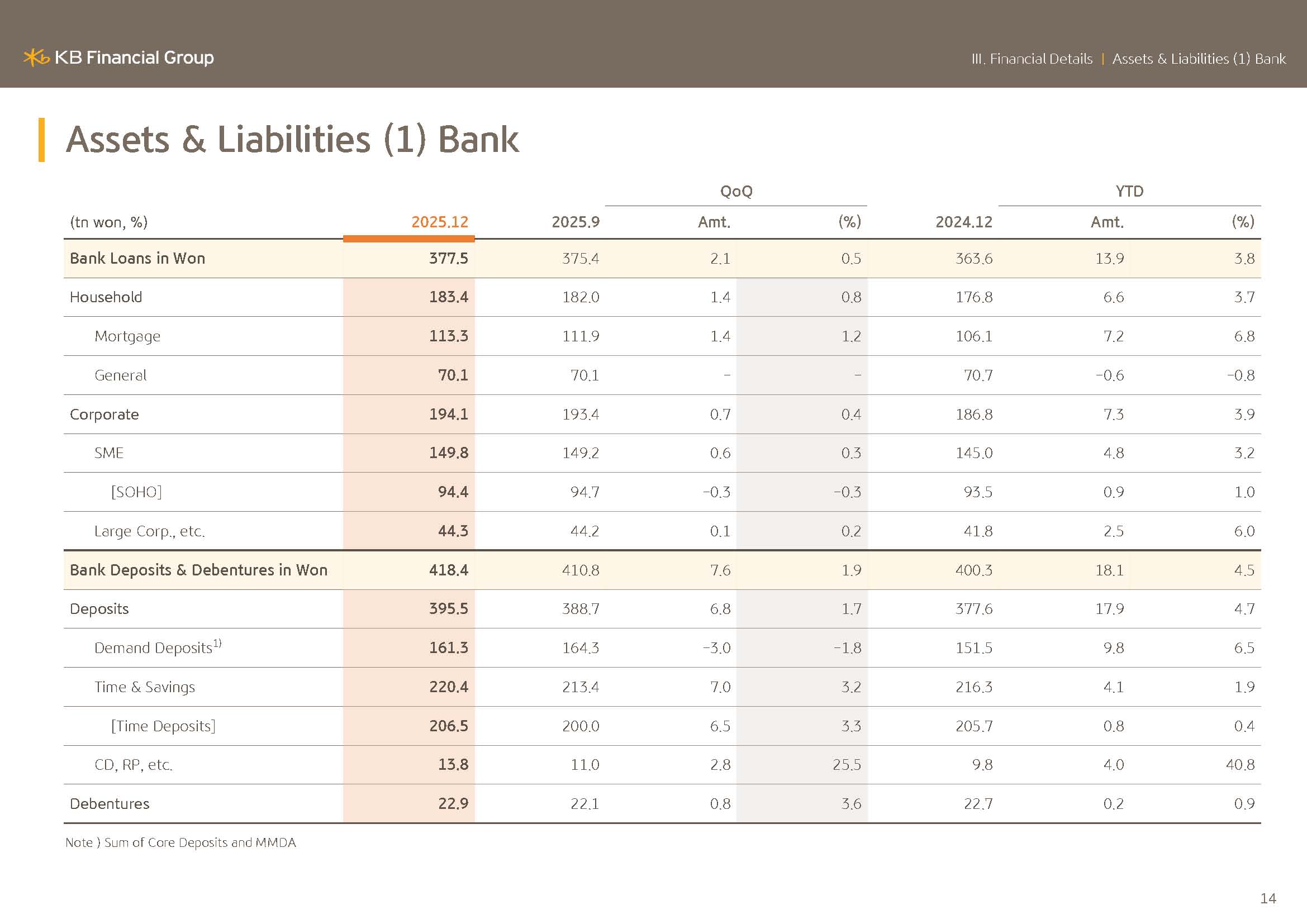

Next, I will discuss the growth of the bank's Korean won loans. As of the year in 2025, the bank's Korean won loan balance did add a KRW377 trillion, representing growth of 3.8% versus year-end of last year and 0.5% versus end of September.

Within this household loans increased by 3.7% versus year-end of last year and by 0.8% QoQ as we pursued growth at an appropriate level under the government's household debt management stance.

While corporate loans grew by 3.9% versus year-end of last year and by 0.4% QoQ supported by the steady expansion of loans to high-quality SMEs and increased lending to large corporates.

Considering government regulations and the slowdown in housing transaction volumes, household lending is expected to show limited growth this year as well.

Accordingly, taking into account factors such as our loan portfolio mixed centered on productive finance, we'll continue to pursue household lending policies focused on improving profitability, and we plan to strengthen the corporate finance, bank-based growth framework by shifting our growth axis toward corporate lending.

Next, let me move to the net interest margin shown at the bottom right.

In 2025, the annual NIM of the group and the bank recorded 1.97% and 1.74% respectively, representing a slight decline from the prior year.

In the fourth quarter, the bank's loan was 1.75%, up by 1bp QoQ as we flexibly adjusted the pace of the household loan growth despite pressure on the loan to deposit spread from the higher deposit rates and reduce funding costs through the establishment of an optimal funding mix, resulting in a slight improvement in them versus the previous quarter.

And this year as well, based on our strong channel competitiveness, we plan to rigorously manage them by increasing low costs deposits and through more sophisticated ALM management.

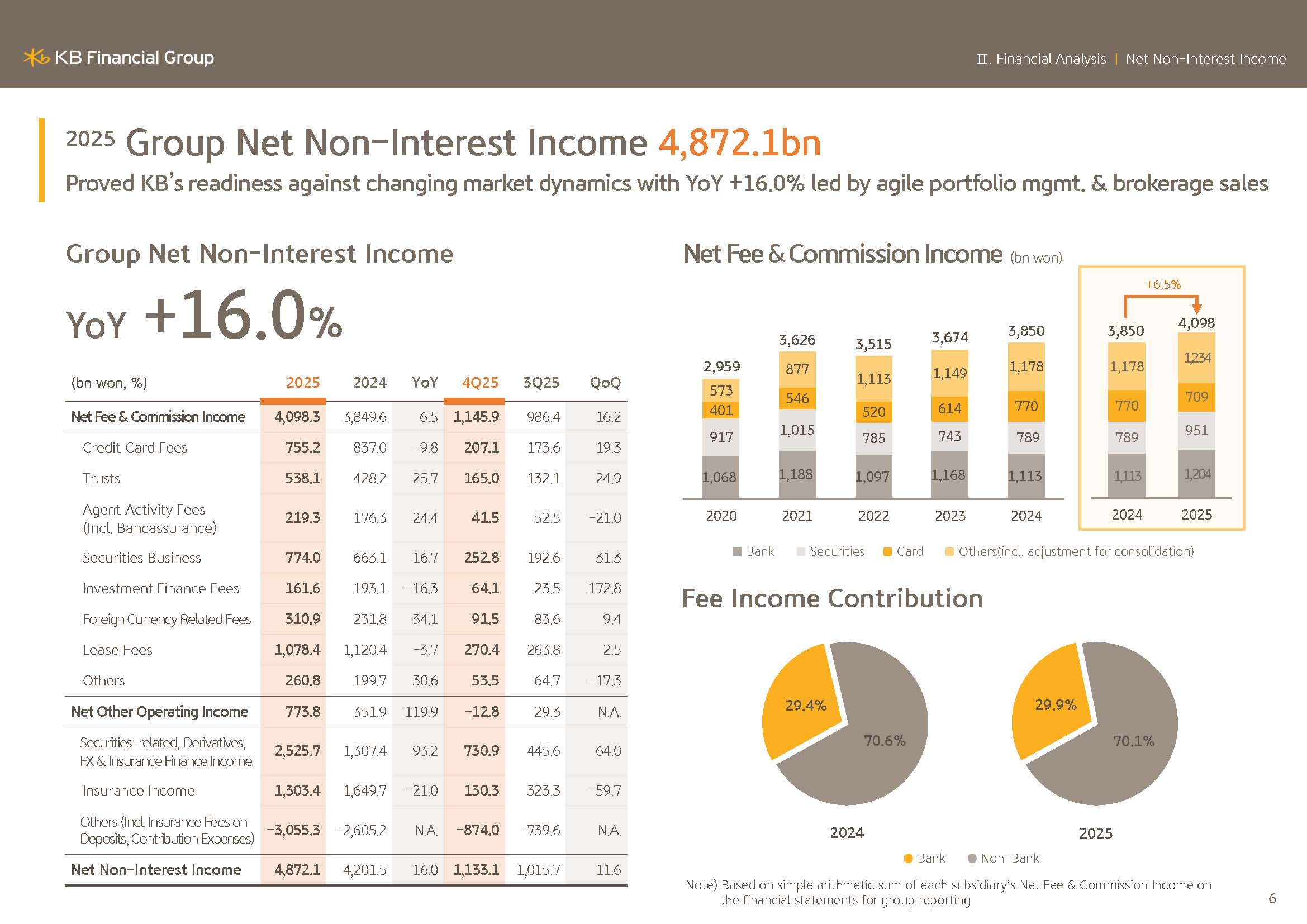

Next, I'll discuss non-interest income.

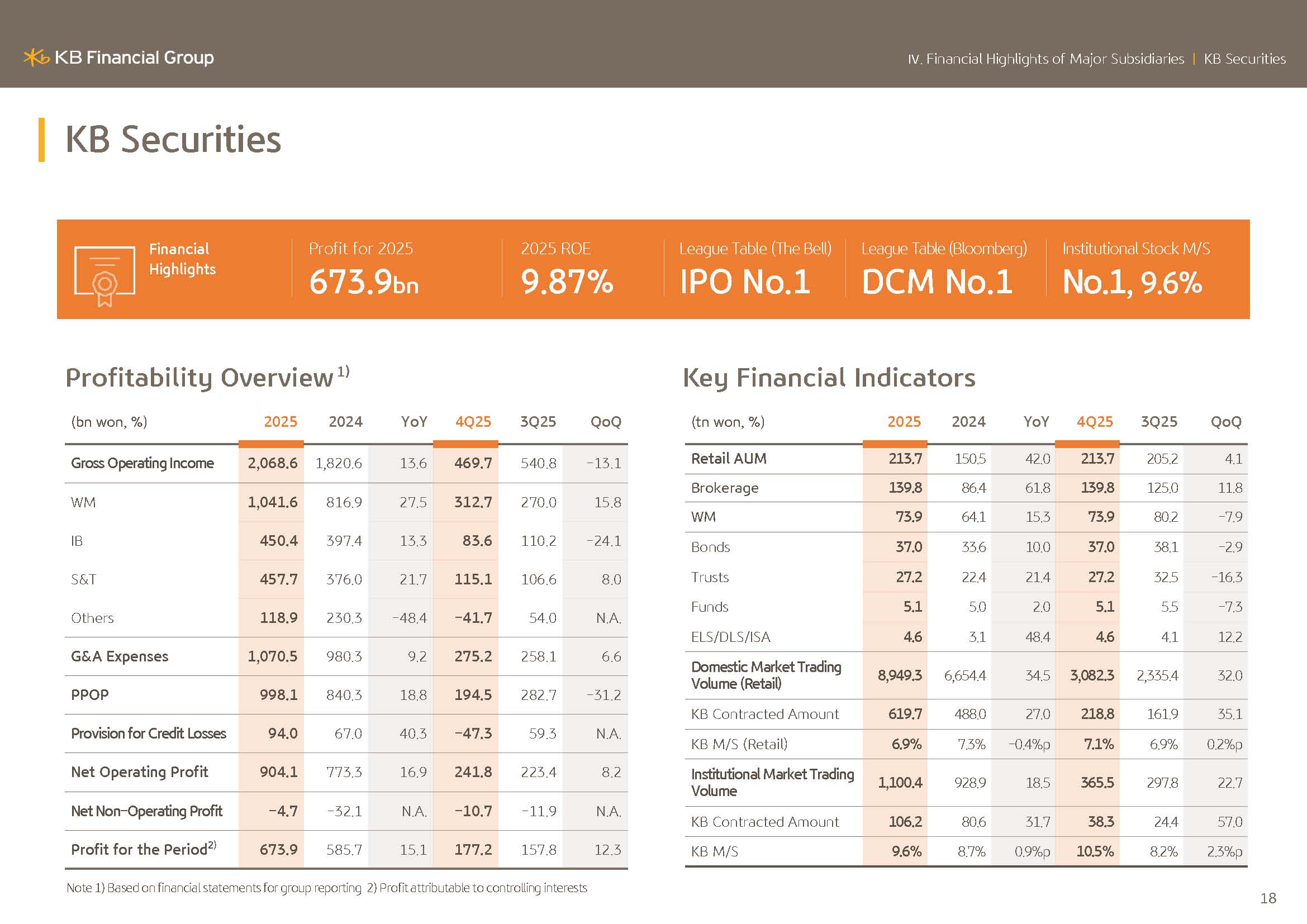

In 2025, the group's non-interest income amounted to KRW4.8721 trillion, expanding sharply by 16% YoY.

In 2025, the group's net fee income was KRW4.0983 trillion, increasing by 6.5% or approximately 248.7 billion.

Compared to previous year, this was driven by a significant increase in brokerage commissions at the securities business due to the expansion of equity market trading value despite a decline in card fees amid the economic slowdown and also by meaningful improvements in the bank's fee income such as banks and fund sales as well as trust-related income.

In addition, capital market affiliates other than securities such as asset management and investment also posted fee income growth of 28.9% and 73.2% respectively, compared to previous year, further supporting the expansion of the group's fee income.

Meanwhile, fourth quarter net fee income is KRW1.1459 trillion reached a record high for the quarter.

Given that non-bank subsidiaries are driving approximately 70% of the groups of fee income, KB will further strengthen the competitiveness of its capital market center non-bank portfolio in line with the government's policy direction to activate the capital markets, thereby further solidifying the fee income base.

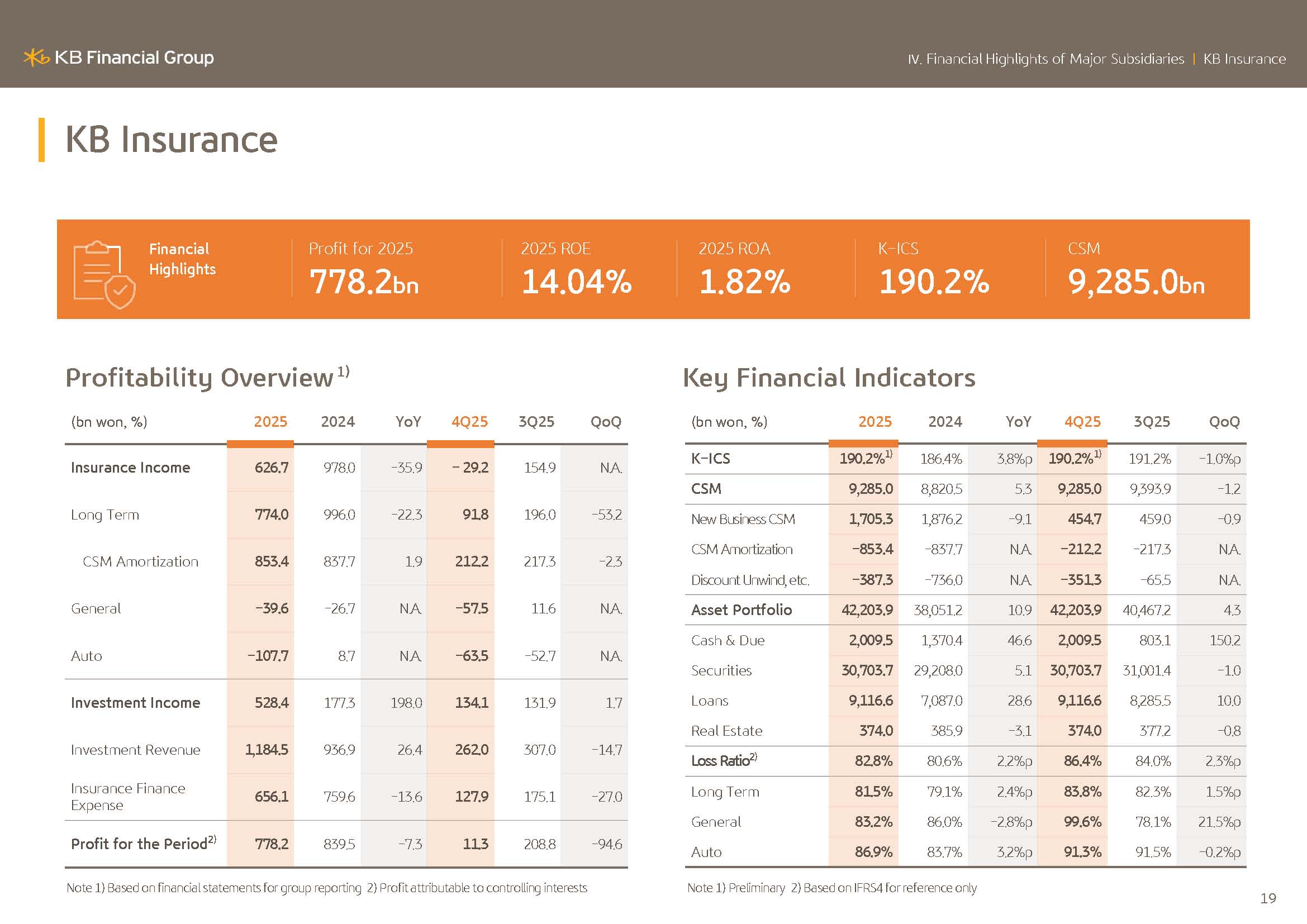

Meanwhile, other operating income in 2025 recorded KRW773.8 billion despite the base effect from the reversal of non-life insurance IBNR reserves in 2024.

It increased by approximately 120% YoY as a result of deficient management of the securities portfolio, including expanded performance from the management of equity securities.

However, in the fourth quarter, other operating income was somewhat weak quarter on quarter due to a decline in the bank income and securities amid a rising bond yields have declined the securities business derivatives income as well.

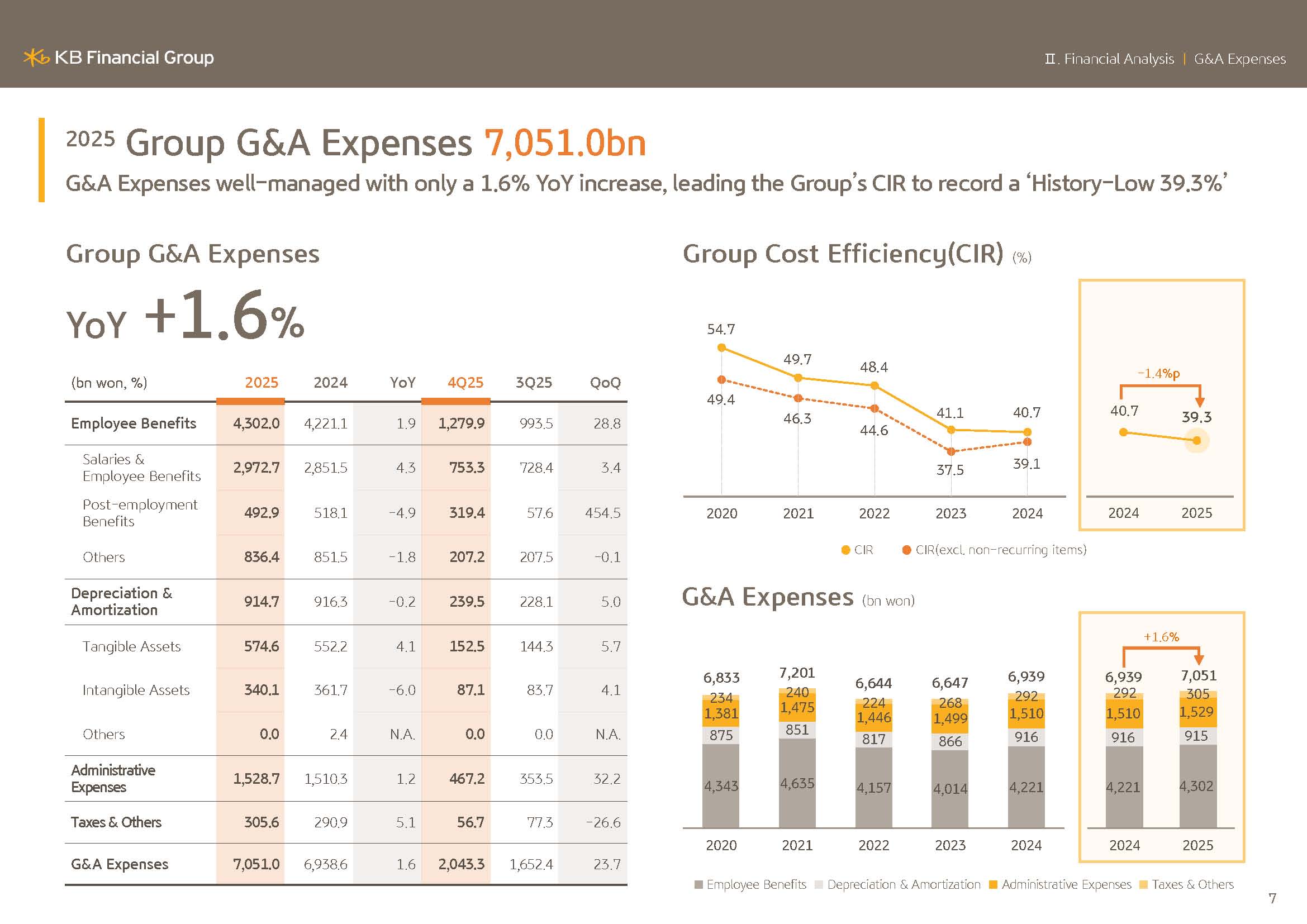

In 2025, the G&A expenses totaled KRW7.0510 trillion, and due to ongoing cost efficiency efforts combined with cumulative effects of the ERP program implemented over the past several years, they increased by only 1.6% YoY.

In addition, the group CIR recorded 39.3% in 2025, reaching an all-time low supported by a solid topline growth, ongoing improvements to our workforce, structure, and cost control efforts. And for the first time in the group's history, coming in below 40% on an annual basis, thereby demonstrating clearly improved cost efficiency versus the past.

Meanwhile, fourth quarter's G&A expenses amounted to KRW2.0433 trillion, increasing sharply QoQ as seasonal factors were reflected, including approximately KRW248.0 billion in groupwide ERP costs in higher advertising and in promotion expenses.

Going forward, the KB Financial Group will expand investments in essential areas such as future growth fields, including AI and strengthening information security, while continuing efforts to reduce recurring expenses in parallel, to efforts to further enhance the efficiency of our, cost structure.

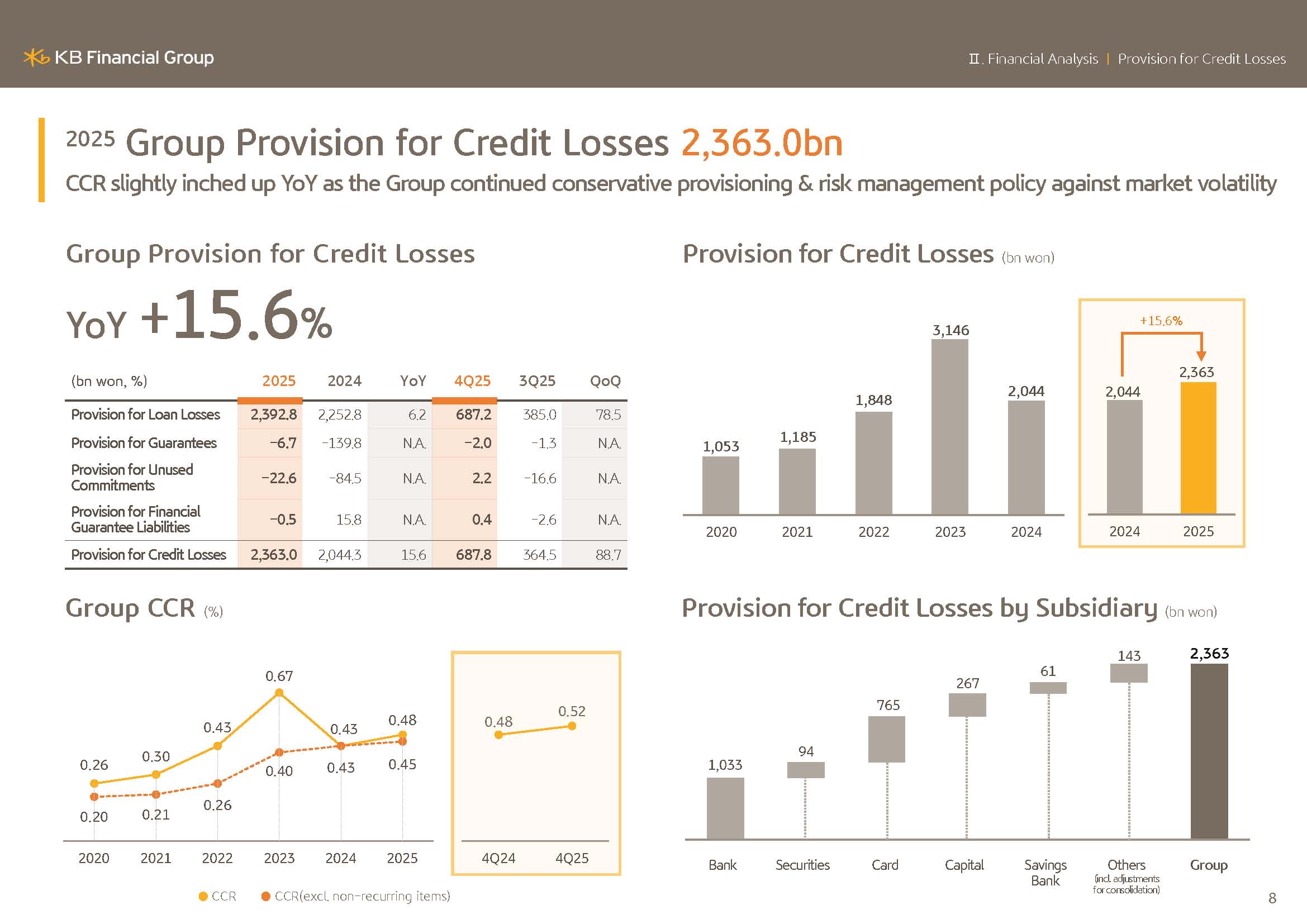

Next is page 8, the group's provision for credit loss.

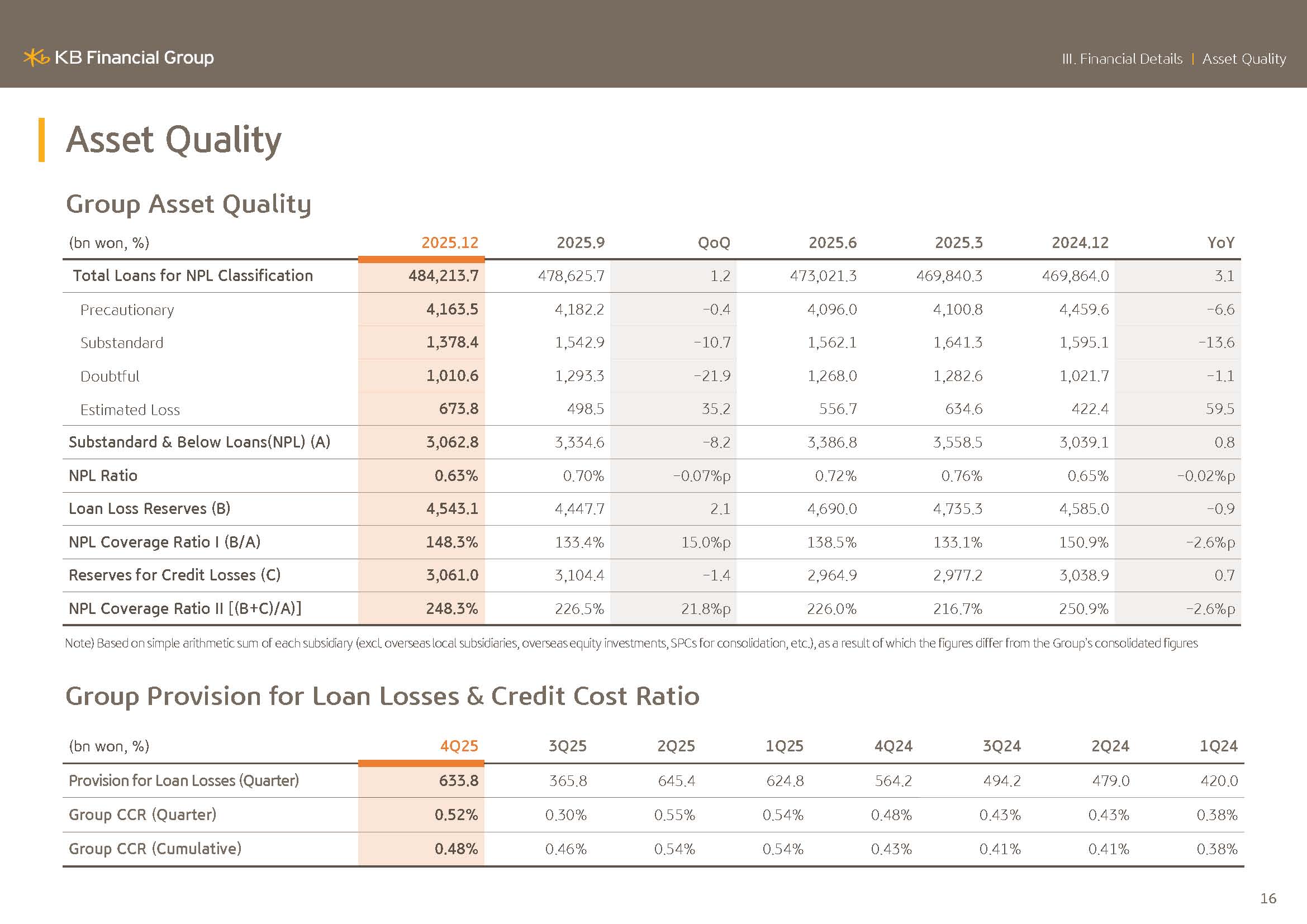

In 2025, the credit loss provision amounted to KRW2.3630 trillion increasing by 15.6% or KRW318.7 billion compared to previous year, and the group's credit costs recorded 48 bps in 2025.

This was despite improvements in asset quality indicators and reduced provisioning burdens resulting from portfolio enhancement efforts. It was due to the maintenance of a conservative provisioning stance across all subsidiaries to prepare for potential economic volatility, including delayed rate cuts.

And as such, we built additional provisions at an appropriate level from the beginning of the year. Based on the loss-absorbing capacity, we have proactively secured and our conservative risk management stance. We expect to manage credit costs stably this year at a level in the low to mid 40 bps range.

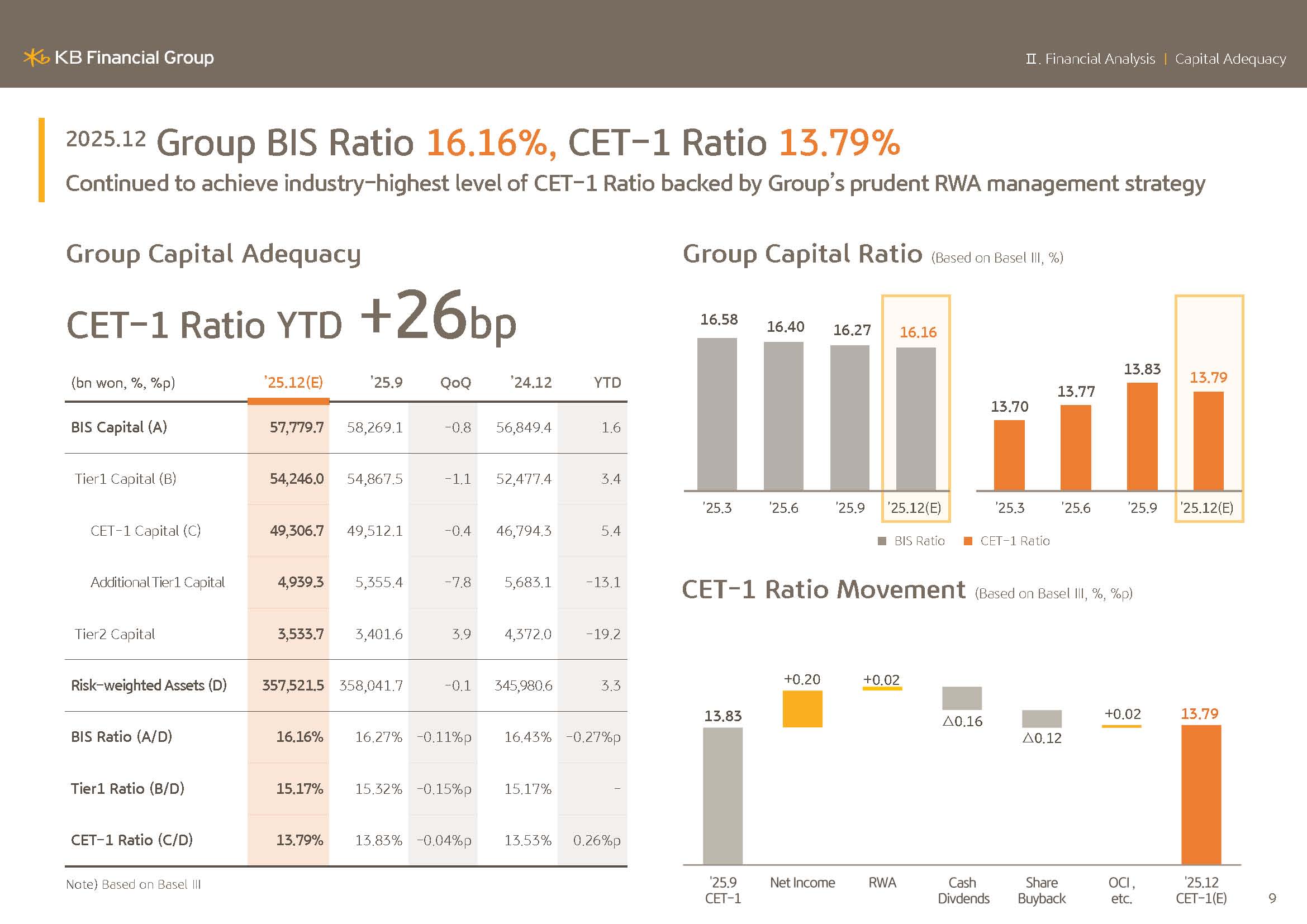

Next, I will discuss the group's capital ratios.

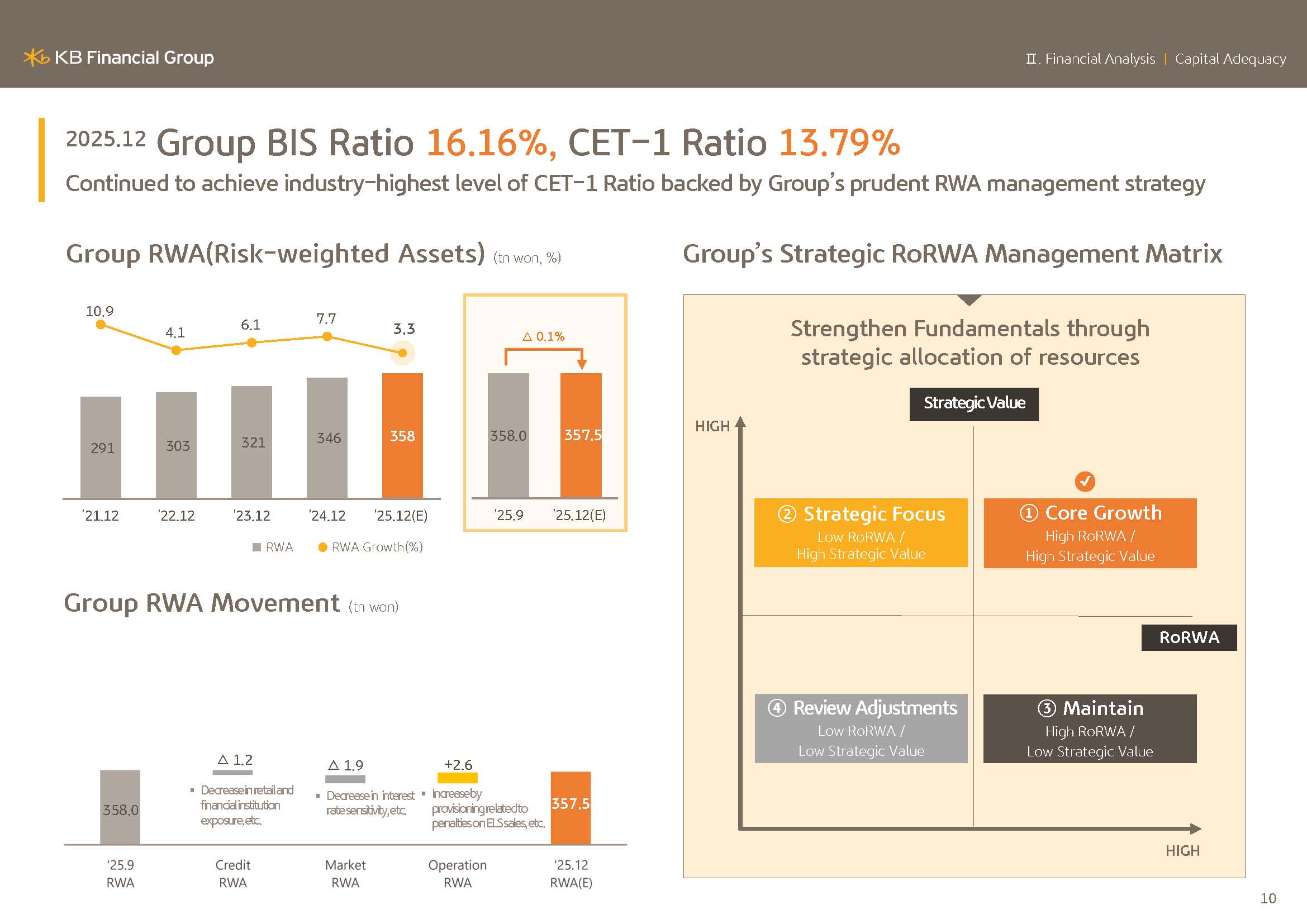

On a preliminary basis, as of the year end of 2025, the gross BIS ratio recorded 16.16% and the CET1 ratio recorded 13.79%, maintaining industry leading capital adequacy despite the downward impact from the increased year-end dividend.

Meanwhile, in the fourth quarter of 2025, the group's risk-weighted assets stood at KRW358 trillion, remaining at levels as similar to the prior quarter increasing by only 3.3% versus year-end of the prior year, thereby growing at an appropriate level within our target range. This year as well, while various factors such as the interest rate and FX volatility may affect the RWA as demonstrated by our 2025 RWA growth rate, we'll continue, sophisticated and thorough group level RWA management strategy, including rigorous limit monitoring and portfolio adjustments in order to manage the growth rate at an appropriate level for the RWA.

From the next page onward, you'll find detailed data on the results explained thus far. So please refer to those materials at your leisure.

With that, we conclude the presentation of KB Financial Group's 2025 business results.

Thank you very much for your attention.